The global dating app industry has matured into a multi-billion-dollar sector underpinned by AI-driven personalization, shifting demographics, and expanding emerging markets. As of 2026, the market is valued between $10.77 billion and $12.52 billion depending on the scope of the estimate, with projections of sustained growth driven by mobile-first populations, deeper AI integration, and rising adoption in Asia-Pacific and Latin America. User growth is slowing in saturated Western markets but accelerating elsewhere. Meanwhile, key players like Tinder, Hinge, Bumble, and Grindr are navigating diverging trajectories — some expanding rapidly, others undergoing strategic reinvention.

Key Trends for Dating Apps 2026 and Beyond

- Quality over quantity: The industry shift is from maximizing swipe volume to driving meaningful matches and real-world outcomes

- Niche dating growth: Apps targeting specific communities (personality-based, religious, LGBTQ+, senior) continue to capture underserved users

- Subscription monetization deepening: Subscription and micro-transaction models are expanding, with revenue-per-payer growing even as total payer counts decline at some platforms

- Video and voice integration: Platforms are embedding video calls, voice notes, and video profiles to drive authenticity and reduce catfishing

- VR/immersive dating: Virtual Reality dating experiences are in early deployment, offering simulated first dates in digital environments

- Digital detox dating: A countertrend is emerging where users seek connections with intentional offline experiences facilitated by apps

- AI companion apps: AI chatbots and companion apps for romantic simulation are growing, fulfilling emotional support needs for users who prefer low-pressure digital connection

- Emerging market expansion: Southeast Asia, India, MENA, and Latin America are expected to drive the majority of new user growth through 2030

Dating Apps Market Size & Growth

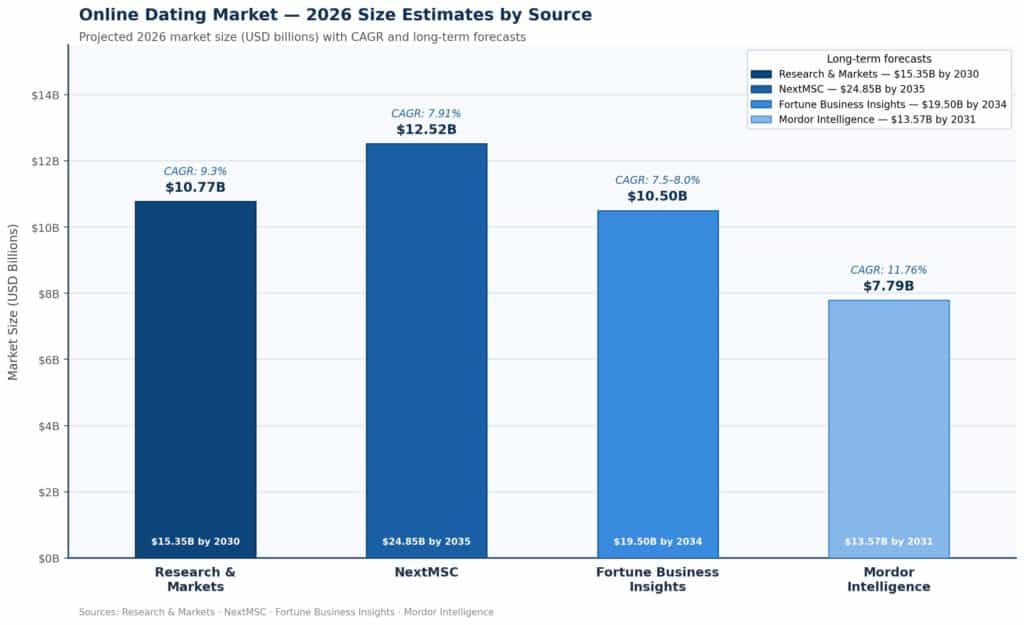

The global online dating market was valued at approximately $9.85 billion in 2025 and is projected to reach $10.77 billion in 2026, growing at a CAGR of 9.3%. A broader definition of the “dating app market” places the 2026 figure at $12.52 billion, with forecasts projecting expansion to $24.85 billion by 2035 at a CAGR of 7.91%. Fortune Business Insights projects growth toward $19.50 billion by 2034 at a CAGR of 7.5%–8.0%.

Mordor Intelligence estimates the 2026 market at $7.79 billion, growing to $13.57 billion by 2031 at an 11.76% CAGR — a more conservative figure reflecting only core online dating services. These variances stem from differing scope definitions (apps only vs. all matchmaking platforms), but consensus confirms a strongly growing industry.

| Source | 2026 Market Size | CAGR | Long-Term Forecast |

| Research & Markets | $10.77B | 9.3% | $15.35B by 2030 |

| NextMSC | $12.52B | 7.91% | $24.85B by 2035 |

| Fortune Business Insights | ~$10–11B | 7.5–8.0% | $19.50B by 2034 |

| Mordor Intelligence | $7.79B | 11.76% | $13.57B by 2031 |

Dating Apps Global User Base

Global monthly active users (MAU) in the dating app industry are projected to exceed 380 million by the end of 2025, rising from approximately 350 million in 2024. The user base is forecast to cross 390 million in 2025, reflecting continued year-on-year expansion.

In total, more than 1.46 billion app downloads were recorded in 2025 across all dating platforms combined. Global in-app spending on dating apps reached $1.45 billion in 2025, driven by subscription upgrades, virtual gifts, and premium feature unlocks.

Key regional and demographic highlights:

- North America: Over 45% of singles have used a dating app at some point

- Europe: 30% of singles engage in online dating

- Asia: ~25% of singles in urban areas use apps regularly

- India: Over 30 million users active in 2026, with the India market valued at $788 million in 2024 and projected to reach $1.42 billion by 2030

- Gender split: 55% male, 42% female, 3% non-binary/other across dating platforms globally

- Age split: 41% aged 18–29, 32% aged 30–49, 22% aged 50+

Dating Apps Platform-by-Platform Statistics

Tinder

Tinder remains the world’s most-downloaded and highest-earning dating app. Key 2025–2026 figures:

- Monthly active users: ~75 million globally

- Paid subscribers: ~9.8 million as of 2025

- 2025 revenue: ~$1.97 billion (estimated)

- All-time revenue: $7.1 billion (as of 2025)

- US market share: 32.32% of the US online dating market

- US revenue share: ~42% of Tinder’s total revenue comes from the United States

- Downloads (2025): ~63 million globally

- Q4 2025 direct revenue: $464 million (down 3% year-over-year)

- Brand awareness: 84% in the United States

Tinder’s user growth has plateaued — paid subscribers declined from 10.8 million in 2023 to 9.8 million in 2025. Match Group has allocated $60 million for AI and product launches at Tinder in 2026, aiming to attract younger users and reverse declining engagement. The app offers 50+ gender identities and 9 orientations; LGBTQ+ users have doubled since 2021.

Hinge

Hinge is the standout growth story of the industry:

- Downloads growth: Up 25% year-over-year

- Q4 2025 direct revenue: $186 million, up 26% year-over-year

- Monthly active users: Grew nearly 50% in European markets throughout 2025

- “Dating Sunday” 2026: Hinge recorded a 31.2% increase in likes and a 24.5% rise in messages vs. an average Sunday

- AI-powered “Standouts” feature: Generated 26% more matches and 2.5× more conversations compared to traditional swiping

- Marriage outcomes: Among couples who met via apps and married in 2025, Hinge leads at 36%, followed by Tinder (25%) and Bumble (20%)

- Revenue target: Match Group aims for $1 billion in annual Hinge revenue by 2027

Bumble

Bumble occupies the #2 position globally and is distinguished by its women-first messaging approach:

- Monthly active users: 50–60 million globally

- Paying users: ~3.6 million as of 2026 (down 16% year-over-year)

- 2025 revenue: Over $980 million

- Downloads (2025): 28.8 million

- Average revenue per paying user (ARPPU): $27.70

- Geographic reach: Available in over 150 countries

- Demographics: 51% of users aged 18–29; 59% of users identify as female

- Daily engagement: ~62 minutes per day average session time; ~49% of users log in daily

Bumble’s paying user base contracted in 2026, reflecting a broader industry challenge of converting free users to subscribers amid economic pressure.

Grindr

Grindr is the clear outperformer in revenue growth among major dating platforms:

- 2025 full-year revenue: $439.90 million (+27.64% growth)

- Q3 2025 revenue: $116 million (+30% year-over-year)

- Q3 2025 adjusted EBITDA margin: 47%

- Full-year 2025 EBITDA guidance: $191–$193 million (43%+ margin)

- Indirect (ad) revenue: Q3 2025 surged 56% year-over-year

Grindr’s profitability and growth distinguish it from Tinder and Bumble, which have seen subscriber declines. The company is investing in AI-driven safety tools and premium feature upgrades, though it faces rising costs and the challenge of evolving AI-enabled scam threats.

Match Group: Parent Company Overview (FY2025)

Match Group (NASDAQ: MTCH), the owner of Tinder, Hinge, OkCupid, and Archer, reported:

- Full-year 2025 revenue: $3.5 billion (flat year-over-year)

- FY2025 net income: $613 million (+11% YoY), achieving an 18% margin

- Q4 2025 revenue: $878 million (+2% YoY), beating analyst estimates of $871 million

- Q4 2025 adjusted EBITDA: $370 million (+14%), 42% margin

- Free cash flow (2025): Exceeded $1 billion

- Total payers (Q4 2025): 13.84 million (down 768,000 year-over-year)

- Market capitalization: ~$7.45 billion

- 2026 full-year revenue guidance: $3.41–$3.535 billion

The declining payer count despite improved profitability reflects Match Group’s strategic pivot from volume growth to revenue-per-user optimization — a notable industry inflection point.

Dating Apps Demographics & Usage Behavior

Age and Gender

- 18–24-year-olds account for ~35% of Tinder users; the average Tinder user age is 26

- 39% of U.S. adults have used a dating app at some point in their lives

- 65% of adults aged 18–29 have used online dating sites or apps

- Among current users, 40% are aged 18–29 and 44% are aged 30–49

- Only 54% of Tinder users are single; 30% are married, 12% are in relationships

App Preferences by Age

- Ages 18–29: Tinder and Hinge dominate

- Ages 30–49: Tinder (46%) and Plenty of Fish (36%)

- Ages 50–64: Match (45%), Plenty of Fish (37%), eHarmony (35%)

- Ages 65+: Match (42%) and eHarmony (32%)

Engagement Patterns

- The busiest day of the year for dating apps is “Dating Sunday” — the first Sunday of January — when swipe, like, and message activity peaks across all major platforms

- Active Tinder users opened the app an average of 4 times per day

- Approximately 1.6 million Tinder users went on in-person dates each week

- Bumble’s most active time is 7 PM in the UK, with similar evening-driven patterns in the US, Canada, and Europe

Dating Apps and Relationship Outcomes

One of the most striking 2025–2026 data points is the conversion of app-based connections into marriages:

- 27% of couples who married in 2025 first met through a dating site or app, according to The Knot’s 2025 Real Weddings Study — the single most common way couples met

- Among app-met married couples: Hinge leads (36%), Tinder (25%), Bumble (20%)

- 1 in 5 adults under 30 say they met their current spouse or partner through a dating app

- 12% of U.S. online daters have entered a committed relationship or marriage with someone they met online

- Couples who met online report higher average marital satisfaction than those who met offline

- 5.96% of marriages that began online ended in separation/divorce, compared to 7.67% for offline couples

- 61% of U.S. adults believe online relationships can be just as successful as those formed offline

- 30% of people who met their partner online report their partner is a different race/ethnicity, vs. 19% who met offline

AI Integration in Dating Apps (2026)

AI is the defining technology trend reshaping dating apps in 2026:

- 72% of dating app users are open to AI-powered features, particularly match recommendations and profile optimization

- Hinge’s AI-powered “Standouts” feature produced 26% more matches and 2.5× more conversations vs. traditional swiping

- Bumble’s “Night In” feature boosted video call conversions by 60% within six months of launch

- Bumble’s “Deception Detector” reduced spam and fake account reports by 45%

- Tinder’s FaceCheck identity verification tool reduced interactions with harmful users by over 50%

- Behavioral-based AI matching can improve user retention by up to 40% by reducing poor-fit encounters

- Match Group has allocated $60 million specifically for AI and product innovation at Tinder in 2026

- Emerging 2026 AI capabilities include emotion detection via NLP/sentiment analysis, voice and video identity verification, and deepfake detection

- AI practice date simulations and gamified “confidence building” flows are entering mainstream apps

Dating Apps Regional Markets

India

India represents one of the fastest-growing dating app markets globally:

- Market size: ~$788 million in 2024, projected to reach $1.42 billion by 2030 (CAGR ~10.65%)

- 30+ million active users in 2026, concentrated in metro and Tier 1–2 cities

- Tinder leads with 20 million+ active users in India; Bumble reports 5 million Indian users

- Android dominates with ~95% OS market share due to cost competitiveness vs. iOS

- Key risk: Rising dating scams — catfishing, financial fraud, and blackmail have grown significantly despite AI verification efforts

Asia-Pacific

Asia-Pacific is the largest and fastest-growing regional user base, supported by rapid urbanization, mobile-first populations, and an expanding middle class. Local apps like Tantan (China), Pairs (Japan), and regional social-discovery platforms compete strongly against Western apps.

Latin America & MENA

Both regions are experiencing rapid growth driven by young demographics and improving digital payment infrastructure. Tinder leads in Latin America, though local apps like Azar compete in the Middle East.

Dating Apps Safety and Cybersecurity

Safety is a growing industry concern:

- 75% of major dating platforms received a grade of D or F for cybersecurity from the Business Digital Index in 2025

- 55% of online daters report encountering a threat (catfish, scammer, identity thief, or aggressor) while using a dating app

- Dating apps store highly sensitive data: private messages, sexual orientation, geolocation, photos, and payment information

- Notable breaches: Ashley Madison (30M users, 2015), AdultFriendFinder (400M accounts, 2016), Coffee Meets Bagel (6M users, 2019)

- API vulnerabilities in Tinder, Bumble, Grindr, and Hinge exposed in 2024, allowing location tracking of users

- Generative AI is enabling more sophisticated romance scams and fake profiles, creating new challenges for safety teams

- AI-based moderation is increasingly deployed as a countermeasure — real-time content monitoring is becoming standard among reputable platforms